Card, mobile credential, payment and security

“The importance of Level 1 document security features cannot be understated … they are the front door locks in any design…” This comment from the UK National Document Fraud Unit succinctly states the importance of Level 1, overt security features to the overall documents security.

We classify embedded card security features – or document security features – into three levels: Level 1, Overt; Level 2, Covert; and Level 3, Forensic.

In a nutshell, Level 1 features are overt and visible to the naked eye. This makes them easy to authenticate by inspectors in the field. Level 2 features are covert, which means they cannot be seen by the naked eye and are only discernable by trained examiners using under magnification or via some other technique tool. Finally, Level 3 features are described as forensic in nature and require trained examiners and complex laboratory equipment for authentication.

ITW Security Division’s white paper on card security features, Level 1 Security – Long Live the King!, focuses on the importance of Level 1 overt features in document security.

An exploration of the specific embedded security features – from holograms and microtext to UV inks and nanotext – for each level is presented in the document. While each feature and each level is important and should be pursued, the crucial nature of solid Level 1 features emerges.

The emergence follows a series of interviews carried out by ITW with leading companies in the security market. These companies spanned 3 continents and included manufacturers, integrators and security printers. Of those interviewed, 100% reported that Level 1 features are in highest demand.

But just as these quickly visible features are becoming more necessary, fraudsters are getting better at counterfeiting traditional Level 1 options. Thus, there is an increasing need for new, advanced document security features that meet Level 1 criteria.

Learn more about document security features in general and explore new options for advanced Level 1 security features in this white paper. It is part of a series of resources on advanced card materials and embedded security features available from ITW. Check it out online.

At the annual National Association of Campus Card Users (NACCU) conference, Bill Norwood was presented with the inaugural award for Lifetime Achievement in the Campus Card Industry.

He spent the first half of his career with Florida State University leading the campus' information technology and computing departments. Norwood launched the pioneering FSUCard program helping to create the framework for the campus card industry and the card model that institutions nationwide would later adopt.

For three decades he assisted many, if not most, of the card programs across the country through his work with the FSUCard, the university's Card Application Technology Center, CyberMark and later Heartland Payment Systems.

Norwood is responsible for a number of firsts in the campus card industry – from ISO numbers and color images on cards, to bank partnerships and financial aid delivery to student IDs. He was one of the five original founders of NACCU, and he enjoyed a long career that spanned both the university and vendor sides of the industry before retiring in early 2017.

For his many contributions, incredible spirit and personal friendship, the CR80News team is extremely proud to honor Norwood with this inaugural award. Hereafter, the award will be presented and named in his honor as The Bill Norwood Lifetime Achievement Award.

Check out the video from the award presentation for more highlights of Bill Norwood’s career.

Hidden below Northeastern University in Boston is a network of tunnels that serve as a passageway for students traversing between key buildings on campus. Unlike the famous tunnels in other cities, these don’t hold catacombs and no Phantom lurks within. Instead Northeastern’s tunnels house one of the world's leading deployments of advanced contactless lockers.

On winter days or rainy evenings, the 16,000 square-foot underground network is particularly appreciated by students. It links 11 major locations above ground, including academic buildings, residence halls, gyms and libraries.

As a part of a facelift that included new energy efficient lighting and colorful directional signage to facilitate travel, the popular – and sometimes hard to obtain – student lockers were upgraded and expanded.

The networked contactless lockers from Gantner Technologies are used around the world at athletic clubs and spas, ski resorts, corporate centers and universities. And in the summer of 2016, Gantner added another university to its user base with the installation of more than 1,200 new lockers at Northeastern.

All 1,286 of the tunnel’s lockers are larger than their predecessors – now 3 foot by 2 foot. Each locker is marked with a letter and number code, identifying its location within the tunnel system.

Students rent the lockers through the university’s myNEU portal and use their student ID – the Husky Card – as the contactless key for locking and unlocking. The lockers are rented on a per-semester basis, and thanks to the Gantner locker management software no staff interaction is required to sign up for or operate a locker.

At the myNEU student portal, all available lockers can be viewed. The student selects the locker of their choice, and the locker is linked to the unique ID number of the individual’s Husky Card. For the remainder of the semester, only that contactless card can provide access to the locker.

The Gantner locking system guarantees the safety of belongings by delivering networked alarms to maintenance and security staff if vandalism is detected. The software also provides locker usage reports, remote locker control and occupancy monitoring.

Today at the National Association of Campus Card Users meeting, CBORD and HID Global announced a new secure issuance service called HID Fargo Connect.

In essence it is a SaaS or outsourced alternative to traditional ID card production. Pulling student data from CBORD’s Odyssey PCS or CS Gold system, the solution prints over the web to Fargo printers located on campus and/or at HID’s service bureau.

According to Lance Johnson, Segment Marketing Manager, HID Global, this does a few key things to ease financial and labor strains on campus card programs. It eliminates the need for a PC to control the printers as this control is handled instead over the web. It also eliminates the need for card issuance software as both card design and production is managed via a SaaS solution.

Multiple printers can also be controlled and managed in a print farm style for large volume on site issuance. As well, large batches can be sent to the HID service bureau and cards will be mailed back to campus when complete.

Much of the control of required components from both the CBORD and HID Fargo sides is handled via mobile and tablets, enabling flexibility in photo capture, card printing and management.

According to Johnson, the solution will be available as via a monthly service fee, encompassing all card stock and consumables, printer replacements, maintenance and even service bureau printing. He says the fees will be very comparable to those spent for traditional issuance environments.

There is one test site now running at MIT, but CBORD and HID are currently looking for additional test sites to rollout this year. Campuses must be CBORD users in the US to apply.

CR80News will cover the project in more detail as information becomes available. Learn more at Hidglobal.com/fargo-connect

A mobile app, some golf carts and a renowned burrito are proving that campus food services can change with the times. Many argue that the traditional model of institutional food service -- student ID cards, board plans with declining balance, on-campus locations and limited availability – can no longer compete in the modern marketplace. But at the University of Arizona, it is not just competing it’s thriving.

Arizona Student Unions partnered with mobile ordering provider Tapingo three years ago in the fall of 2013. “We were responding to the lines,” explains Todd Millay, interim director for UA Student Unions, referring to the campus’ ever-growing food queues.

Millay oversees 30 retail outlets on the Tucson campus and serves between 25,000 and 30,000 meals per day. “Everyone still eats at the same time, so with mobile ordering, we were trying to be responsive to lines,” he says.

It’s a sensible strategy, because if you can increase throughput at the moment when lines normally become problematic, then students won’t walk away and go to your competition.

“How do we maximize the same six registers at the Chick-fil-a?” he asked. It was the kind of question that led to the mobile ordering trial.

Since that successful trial three years back, mobile ordering has expanded to 80% of the university’s retail outlets. As Millay explains, the solution is best suited to declining balance users and locations that service them. Board plan users and more traditional dining hall locations don’t benefit from mobile ordering to the same degree, as they tend to be eat-in and self-service in nature.

Enter the Highlands Market breakfast burrito, a staple of any Wildcat’s life.

“The ticker machine never stops,” says Millay, referring to the printer that pushes out Tapingo orders in the Highlands Market kitchen.

This hints to the advantage of mobile ordering. The receipt ticker tells the kitchen that someone wants to pick up a burrito soon, and while they’re not standing at the counter right that second, they will be in a specified number of minutes. These minutes are the key to reducing the lines Millay mentioned, increasing throughput and enticing customers to come back for more.

“We call it the anticipation throttle,” he says. “Getting the order to the staff 14 minutes earlier gives us time to prepare.”

It seems to be working. Across the university’s outlets, mobile ordering already accounts for 15% of all orders.

Ultra-violet (UV) inks let passport and card issuers embed strong security features into the identity document itself. UV printing is considered a Level 2 – or covert security feature -- because the images are not visible to the naked eye. Instead, they only emerge when a UV light source is present.

ITW Security Division recently released a new embedded security feature that uses UV ink and is uniquely designed to deter counterfeiting of passports, ID cards and other secure documents.

Called Imaprotek, it is a multi-color photographic image that is printed using special UV inks. The detailed, vibrantly colored image is completely invisible under normal light but is vivid when viewed under either UV-A or UV-C light.

“UV prints are an integral part of today’s security documents … that help international law enforcement and border authorities establish their authenticity,” Says Bob Carey, ITW Security Division’s Business Unit Manager.

Here is an example. Take a picture of a country’s national bird, print it using UV ink and embed it into the passport page or card. It adds a strong feature that makes counterfeiting difficult but is still readily detectable to document verification officials in the field.

ITW makes UV printed images even more secure by fusing the Imaprotek image into its Fasprotek security laminate.

Fasprotek is an ultra-thin laminate that can applied onto passport pages or cards to protect the underlying data and add additional embedded security features including OVDs, UV printing, metallic printing, tactile features and many other options.

The combination of the image and laminate adds key security advantages for issuers. First, because the image is built into the laminate it is virtually impossible to alter. Such attempts are immediately obvious thanks to the product’s frangible layers.

Second, because the Fasprotek layer does not block UV light from passing through, the Imaprotek images can be layered on top of other UV printed security elements below the laminate.

Returning to our example, the national bird could be visible using UV-A light in the laminate layer, while another embedded UV image or UV security text could be visible directly beneath it using UV-C light. This layering of covert security features is extremely difficult to fake yet still very easy to verify.

Often protective laminates obscure UV printing below them, and thus negate the value of these security features on variable data pages.

“We have been able to combine the UV security of Imaprotek and protection of Fasprotek to provide an integrated security solution that ensures UV-C is clearly and vibrantly visible across the security document,” says Carey.

In a free on-demand webinar, campus card vendor Blackboard Transact explores the move to student attendance tracking in higher ed and demos its new automated attendance application.

In a free on-demand webinar, campus card vendor Blackboard Transact explores the move to student attendance tracking in higher ed and demos its new automated attendance application.

Automated, card-based solutions for attendance tracking are becoming more common in higher education. Financial aid and other reporting requirements are pushing campuses to track attendance and institutions are striving for ways to increase student success, retention and matriculation.

Blackboard Attendance uses your existing student ID card -- from any campus card vendor – as the tool to track attendance. A small mobile card reader syncs with iOS or Android handsets and tablets to make attendance data available in real time for instructor viewing and future reporting.

It’s cloud-based, SaaS architected and easy to setup and deploy. In this informative webinar, hear Blackboard representatives how institutions and students alike can benefit from automated attendance tracking.

Watch the free, on-demand webinar by clicking here.

It was more than three years ago that US PIRG released its report damning the relationships between financial providers and academic institutions that provided payment card products to students. In its wake, other reports from the agencies like the Government Accountability Office, Congressional hearings and consumer protection efforts followed. Then came the Department of Education's efforts to revamp financial aid disbursement.

The DOE convened a 2014 Negotiated Rulemaking Process to gather input from a cross section of concerned groups. After months of meetings and drafts, negotiators reported that they thought they had successfully re-crafted the rules. But representatives from industry and the consumer advocacy groups failed to reach total consensus, leaving the DOE free to draft the rules as they saw fit.

In mid-May, the DOE’s final proposed rules were released, and they are not favorable for industry, campus administration or even students. They appear to be a win only for the consumer advocacy groups that have been pushing to have banks and payment cards completely removed from the process.

Since the Negotiated Rulemaking began, both the service providers and the campuses relying on them to disburse financial aid to students have been on proverbial pins and needles. The future of this line of business and peripheral services -- such as campus card and bank partnerships that deliver accounts and debit cards to students -- have been up in the air.

I have written about this many times before and have worked with associations, providers and campuses attempting to plan for the future. The goal has been to help the DOE develop productive regulations that protect students and grow these services. But from the beginning, the car has been driven by consumer advocacy bodies that seemed devoted to the banishment of these relationships from higher education.

Still I always believed that cooler heads and data-driven decision making would prevail. After all, I know that the vast majority of these services are beneficial for campuses and students alike – better in most cases because the campus is involved on the student’s behalf.

I kept this cautious optimism throughout the negotiated rulemaking process, loads of phone briefings, several years of conference sessions and a series of draft proposals and comment periods.

I am no longer optimistic.

I fear that the draft regulations released by the DOE in May are likely to pass without significant changes. I have heard no insider intel to suggest that the comment period that ends on July 2 will produce substantive change.

For the first time, this has me thinking about worst-case scenarios. What if the consumer groups get their wish and some or all of these relationships that both campuses and students rely on actually do go away?

As both a student and a university employee, I remember the “net check” process where everyone receiving aid had to get it via paper check. It was painful on both sides. Are we destined to relive it? As other federal programs from Social Security to Veterans Affairs totally eliminate checks, is the DOE pushing campuses backward?

Do they think forcing campuses to manage ACH processes in-house, increase the use of paper checks and push students to use their existing bank accounts really solves a problem students are facing? Many paper checks will be cashed at rip-off payday loan shops. The students’ preexisting bank accounts all charge non-sufficient fund and other traditional fees the DOE is trying to eliminate.

Sadly, many of the products the new regulations will curtail actually are better, as they offer low- or no-fee alternatives that help students access Title IV funds. In the rush to appease the consumer advocates, it seems the DOE has overlooked this reality.

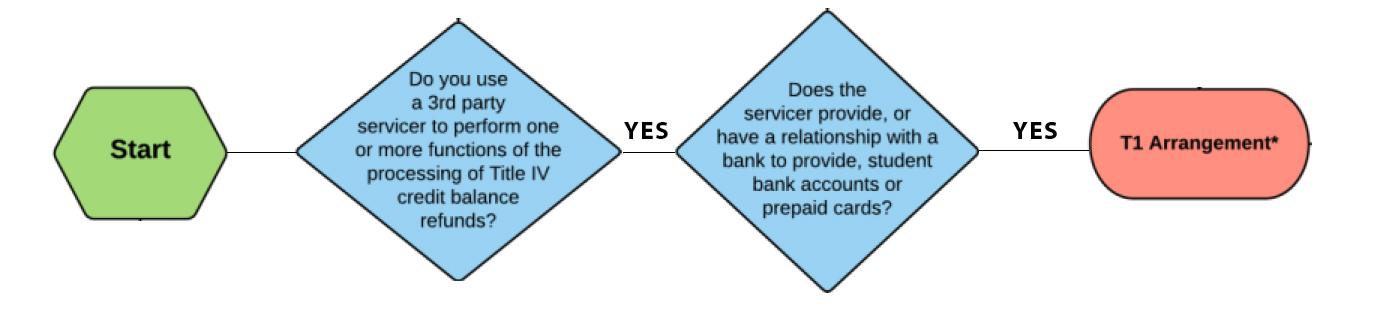

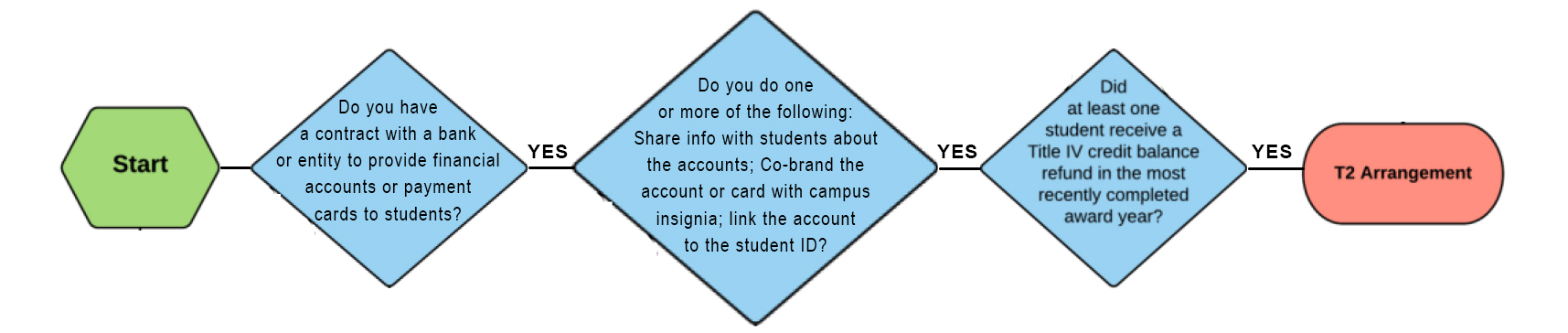

NACUBO created a flowchart to enable a campus to determine whether or not they have a T1 or T2 relationship. In the interest of getting down to layman terminology and simplifying the subject, we have abridged that flowchart to a more basic version.

Do you have a T1 provider?

Do you have a T2 provider?

Lets make some assumptions and head down the path of worst-case scenarios. Assume that the proposed rules pass without substantive change or perhaps get even more punitive toward T1 and/or T2 entities. What might the implication be for your campus?

To state the question another way, “what if my provider goes away?”

A recent US Senate Banking Committee hearing addressed issues that could determine the future of campus card bank partnerships. Though many expected ID cards and aid delivery to be a minor topic in comparison to other Title IV financial aid related issues, it dominated much of the discussion during the hearing titled “Financial Products for Students: Issues and Challenges.”

The following article highlights key testimony, including an opposition letter from the seven Kansas state system institutions, a US PIRG representative outlining the consumer advocate position against these accounts, and finally a banking association president’s case for the positives provided by bank and campus partnerships.

A video of the hearing and testimony is available at the following link. Jump 17:00 minutes into the video coverage to listen in on card-related issues. (http://www.banking.senate.gov/public/index.cfm?FuseAction=Hearings.LiveStream&Hearing_id=8058e98c-2c38-4e5c-999a-fdae0e929bc4)

At the start of the hearing, US Sen. Jerry Moran, R-Kan., read a letter submitted by the presidents of seven institutions in the Kansas state system. It stated their concern with language that regulates any arrangement in which a student opens an account into which the Title IV funds are to be placed.

Senator Moran read from the letter for the Kansas Universities:

“(This regulation) could have a chilling and in some cases terminal effect on good business partnerships that currently benefit students and universities alike.

Students often far from home need access to safe and secure financial services. Financial experience is a necessary part of student life and is essential training in long-term financial health.

Knowing this many schools have signed agreements with banks to provide on-campus financial institutions at low or no cost students. Such services include secure on-campus branches, ATMs, debit cards and financial education programs.

Any regulatory action that could potentially take away students safe convenient and free access to one group of essential services while it simultaneously drives up the cost of education for that same group of students deserves to be studied with extraordinary care.”

Christina Lindstrom, US PIRG spokesperson, highlighted what the consumer group sees as unfair and onerous for students:

“Right now students are being hit with high fees that are hard to avoid as they try to access their federal financial aid refunds through campus sponsored bank accounts and prepaid debit cards. We found in our 2012 report, “The Campus Debit Card Trap,” that two in five college students in the country are exposed to debit cards on campus that may drive up their costs.

Students at some campuses are charged steep and unusual fees to get to their federal financial aid including PIN transaction fees at the point-of-sale, overdraft fees of $37 or more. On the whole these accounts are not necessarily a better deal for students than what they might find through a bank not affiliated with the campus.

Still industry-leading banks and financial firms can see 40-75% of students on a campus using the campus-based product a few years of marketing. How do they do it?

First, banks and financial firms behind these products often rely on multi-million dollar revenue-sharing agreements with campus administrations. The contracts include receiving direct payment to use the school’s logo, providing bonuses for recruiting students and discounted pricing in exchange for marketing access.

In addition they used push marketing and other strategies to steer students into opening up these new accounts over using their existing bank accounts.

Higher One, a prominent financial firm in this market, pre-mails the cards to every student on campus, before they’ve opted in or out. The cards are co-branded with the college logo giving impression that the student must open the account.

At another college, bank representative actually set up tables right outside the student ID office, essentially … aggressively promoting their accounts that students can link to their id cards. Students can get freebies like bags and T-shirts for signing up.

Finally the fees can be high as I mentioned and unusual. Fees on university-sponsored cards include a variety of PIN swipe fees, inactivity fees, overdraft fees, ATM surcharges, fees to reload prepaid cards, fees to check your account balance … I could go on. The fees can be hard to avoid, for example, if a merchant only accepts PIN debit or there’s no fee-free ATM available.

All campus bank accounts and prepaid card services can charge overdrafts. Overdraft coverage is a form of credit since the financial institution covers the consumer shortfall and subsequently repaid the amount extended plus a fee. Some banks engage in the abusive practice of purposefully reordering transactions to maximize overdraft fees. Many banks and financial firms that are playing on campus right now have been held accountable for their abusive practices in this arena.

Overdraft fees are inconsistent with the Department of Education’s existing rules on school-sponsored accounts. Department of Education rules also require that students be provided convenient fee-free ATM access. In practice access can be limited.

One argument that’s being made in defense of these campus banking products is that too many low income students are not able to acquire a bank account other than on campus – these are the unbanked students. The Consumer Financial Protection Bureau found less than one-half a percent of college students in America are legitimately unable to secure a bank account, so new student who comes on the campus without a bank account – she doesn’t have one because she chose not to have one or she hasn’t gotten one yet.

Students do not need campus-sponsored bank accounts.

So I urge you to consider legislation that bans revenue-sharing agreements between colleges and banks or financial firms crafted specifically to offer bank accounts and related banking products to students on campus. The conflict of interest inherent in these accounts is problematic for the student consumer and it needs to be addressed.”

Richard Hunt, President and CEO, Consumer Bankers Association articulates the case for continuation of these relationships and accounts:

Some Consumer Bankers Association members have entered into agreements with institutions of higher education to provide useful services, such as campus ID cards that can be linked, at the option of students, to a standard deposit account. These financial institutions also provide important services, such as on campus financial literacy programs and assistance with financial aid systems to colleges and universities.

According to a GAO report, “Most of the college card fees we reviewed generally were not higher, or in some cases were lower, than those associated with a selection of basic or student checking accounts at national banks. In particular, college card accounts generally did not have monthly maintenance fees, while the basic checking accounts we reviewed typically did.”

Recently, the DOE entered into a negotiated rulemaking with a variety of stakeholders, including students, school representatives, banks, credit unions, consumer groups, and others, on the topic of “cash management,” which includes the disbursement of student aid refunds, federal aid in excess of what is needed to pay school charges. Despite significant progress among non-federal negotiators and the offering of good-faith proposals by the bank and credit union negotiators, consensus proved elusive. This leaves the Department unbound by any agreements worked out during the negotiations, and free to write whatever changes to the regulations it wishes to propose.

CBA shares the DOE’s goal of promoting students’ understanding and management of financial products while ensuring they have meaningful choices. However, we have serious concerns about and objections to the expansiveness of the draft regulation related to disbursement of federal student aid credit balances, particularly with regard to non-disbursement accounts (i.e. accounts opened outside of the Title IV credit balance disbursement process), as well as sponsored disbursement accounts. Similar apprehensions relating to the scope of the DOE’s rulemaking have been expressed by members of both parties and houses of Congress.

With regards to non-disbursement accounts, though the language in the draft regulation presented by the DOE during the negotiated rulemaking is not clear, it would certainly classify as “sponsored accounts” any traditional bank deposit account linked to a “campus card,” such as a college identification card, even though the depository institution offering the account does not facilitate the delivery of federal student aid credit balances for the school – which is the true subject of the rulemaking. In addition, the draft regulation could cover any deposit account that could receive federal student aid credit balance disbursements held by a financial institution that happens to have other types of arrangements with colleges or universities (“educational institutions”). As sponsored accounts, these accounts would be subject to various requirements and significant restrictions under the proposed regulation, impacting relationships that have nothing whatsoever to do with the disbursement of federal student aid credit balances.

While the DOE has authority to write rules concerning Title IV financial aid disbursement and the methods under which disbursements are made, the proposed rule would go beyond that scope and regulate the availability and terms of deposit accounts, including debit cards and prepaid cards, available to students from depository institutions – separate and apart from the financial aid disbursement process. We can identify no authority for DOE’s overreach to regulate deposit accounts that have, at best, only a tangential relationship with those accounts.

Moreover, and more importantly, this broad scope would have a chilling effect on the offering of accounts designed for students and would deprive students of choice and access to valuable, low-cost, and convenient access to bank services, accounts that can be especially useful to those students who arrive on campus without a bank account. For these reasons, we have urged the DOE to reconsider its draft regulation so it does not cover these traditional bank products and services to the extent they are offered outside of disbursement services (i.e., to the extent the deposit account opening process is not integrated within the federal student aid credit balance disbursement process).

In addition to our concerns regarding non-Title IV disbursement accounts and services, we are concerned the proposed regulation will effectively eliminate federal student aid credit balance disbursement accounts — that is, accounts specifically designed to disburse federal student aid credit balances—to the detriment of students and educational institutions.

Federal student aid is disbursed directly to colleges and universities, which use the funds to satisfy a student’s tuition expenses and then disburse the remaining funds to the student to be available for other appropriately related purposes. The DOE has issued a series of student aid credit balance disbursement regulations, which have increased the operational complexity of disbursing these funds to students. Financial service providers have partnered with educational institutions to help these educational institutions satisfy the DOE disbursement requirements. These arrangements enable colleges and universities to reduce the costs of disbursing federal student aid credit balances by utilizing direct deposit, rather than mailing paper checks, thereby decreasing costs for students and schools and provides to students, safe, quick, and convenient access to funds. In some of these arrangements, financial institutions may offer students a deposit account within the credit balance disbursement process itself or, when instructed by the educational institutions, provide them with a prepaid card to access federal student aid credit balances, particularly where a student does not have a pre-existing account to accept a direct deposit of funds. Most importantly, these products and services are always offered as options and are never a requirement. As evidenced by the chart below, institutions of higher education offer students a variety of options for receiving excess student aid funds. Paper checks along with ETFs to a bank account of the student’s choosing are the most prevalent methods for disbursing these funds.

For those students who do not have, or cannot easily access, an existing bank account, a letter from the National Association of College and University Business Officers (NACUBO) notes, “campus banking relationships can streamline the process of establishing a new account or a pre-paid card option provides an alternative to a check.”

The draft regulation presented by the DOE during the aforementioned negotiated rulemaking would effectively deprive students and educational institutions of these services by compelling financial institutions currently providing such “sponsored accounts” – including those in no way opened in connection with the credit balance refund process – to stop providing them to tens of thousands of students on multiple campuses. Draft regulation would restrict nearly all income sources associated with the maintenance and use of these products. With limited or no means to support the cost of providing the services, providers may have no choice but to exit the business and close existing accounts.

The result would be thousands of students losing a convenient, safe, and quick option to access their federal student aid credit balances, and the convenience of a single card that – at the election of the student – can combine financial and school functionality. Payments to students via checks would be more prevalent, especially for those without bank accounts, delaying the students’ access to the funds and potentially causing them to incur off-campus check cashing fees. In addition, it is worth noting the CFPB found that requiring disbursement through electronic fund transfer can reduce fraud and costs.

CBA is hopeful all involved in this process come to understand how banking relationships on campus provide students access to a range of financial products and options to meet their needs. It is especially important that the function of providing general financial services is not adversely affected by concerns over the separate issue of making federal aid funds available to students who wish to have funds deposited directly into a bank account, instead of being given cash or a check.”

CR80News learned that NuVision’s President, Bill Adoff, and Vice President of Sales and Marketing, Brian Adoff, are no longer with the company.

Bill joined the company back in 2001 and has held various roles related to operational management and product development. Brian Adoff joined NuVision in 2007 and served as national sales manager prior to his current role. In response to CR80News’ request for comment, Brian Adoff responded via email.

He said, “although Bill and I have served as the face and driving force of NuVision for the past five-years, we are no longer partnered with NuVision due to differences between ourselves and the other members as to the direction of the company.”

Company representatives have not yet responded to our request for comment.